2024 – Looking backwards and forwards

Over the longer term, investors expect a positive, after inflation return from investing in company shares and lending money to governments and companies by owning bonds. Unfortunately – and inescapably – in the shorter-term market returns are anything but predictable. They contain a lot of noise, as the market absorbs new information into prices. High inflation in 2022 led to a rapid rise in interest rates around the world, contributing, in part, to the fall in global bond and equity prices. It was a painful backward step and a reminder that the road to long-term returns can be bumpy and painful at times. With these now higher yields, some investors may have been tempted to hold more cash but roll forward a year and that would have been a poor decision in the short term. It is nearly always a bad decision in the long term for those with long investment horizons. Fortunately, 2023 has delivered a much more positive story.

Looking backwards

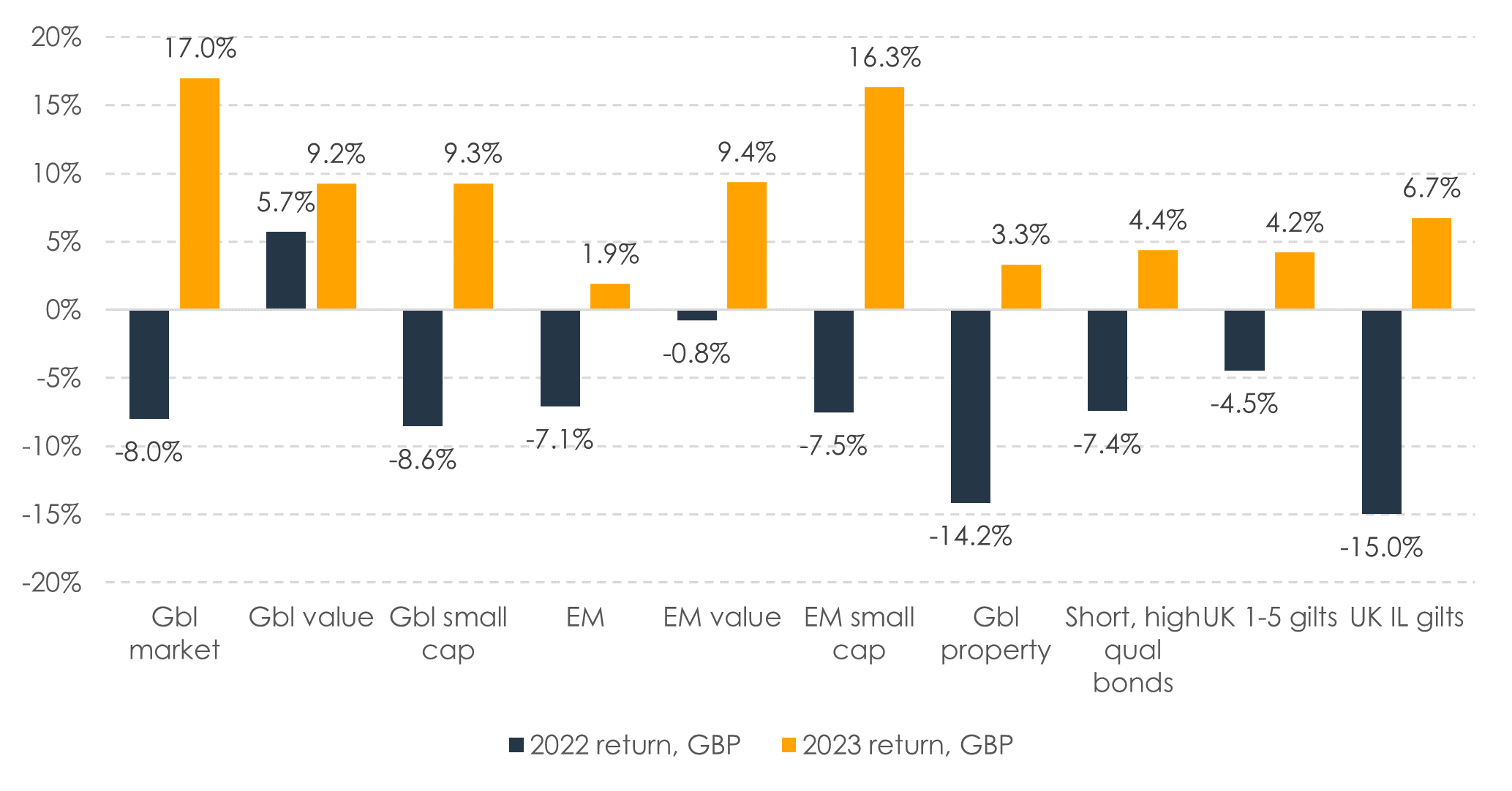

Last year all core assets delivered positive returns. The US market – and in particular the ‘Magnificent Seven’ as the press have dubbed the big tech firms – regained the losses they suffered in 2022. In fact, they contributed around three quarters of the return of the US market over the year. As a consequence, global developed market returns were very strong, given that the US weight in global markets is around 63%. Value companies underperformed in the US (largely because of the overwhelming impact of the ‘Magnificent Seven’) but made a strong contribution outside the US. Both value and smaller companies outperformed strongly in emerging markets. Global commercial property (REITs) also managed a positive return.

On the defensive side of portfolios, high quality, short-dated bonds have recouped over half of the falls suffered in 2022 – largely on account of the higher bond yields, which caused the pain in 2022 – delivering returns similar to cash.

Figure 1: Global investment returns – 2022 and 2023 compared

Data: Funds used to represent asset classes, in GBP. See endnote for details.

Data: Funds used to represent asset classes, in GBP. See endnote for details.

Sensible, systematic portfolios comprising a diversified ‘growth’ basket of equities – with tilts to value and smaller companies – paired with ‘defensive’ short dated high-quality bonds will have delivered robust returns in 2023, somewhere in the region of 9% for a 60/40 split respectively in GBP terms . Investors with portfolios denominated in GBP suffered a small currency drag over the year as Sterling appreciated against the US Dollar by around 4%, as well as most other major currencies. Year-on-year inflation in the UK fell to 3.9% in November, down from 10.5% at the start of the year.

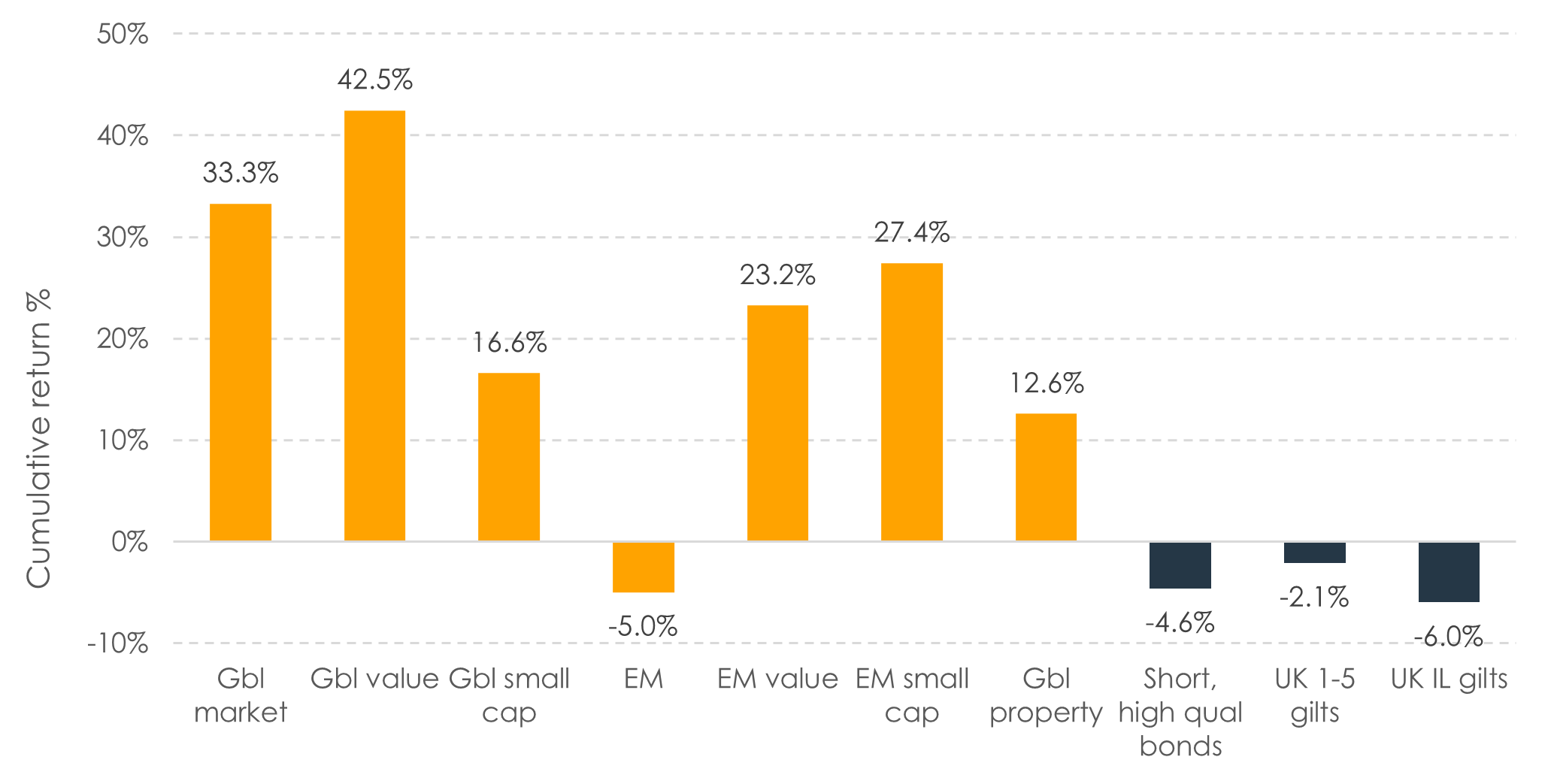

Looking at three-year cumulative returns helps to illustrate the benefit of remaining invested through tough years such as 2022. Bond returns have been poor due to starting yields around 0% at the start of the period followed by subsequent yield rises (and thus bond price falls), but these were more than compensated for by strong growth asset returns.

Figure 2: Cumulative global investment returns – three years to the end of 2023

Data: Funds used to represent asset classes, in GBP. See endnote for details.

Data: Funds used to represent asset classes, in GBP. See endnote for details.

Looking forwards

The outlook for the global economy looks a little bleak as major economies teeter on the brink of recession, including the UK. China has deep and wide economic problems that are restraining its growth prospects. Inflation has come down in the EU (2.4%), US (3.1%) and UK (3.9%) from recent double digit highs. Risks remain – including conflict in the Middle East impacting energy and supply chains –and the final yards to reach central bank target levels of inflation (2% in the UK) will be harder to achieve and vulnerable to geopolitical risks. Interest rates may well remain elevated relative to the low rates that investors experienced up until early 2022, which is good for bond holders.

It is useful to remember that forward-looking views are already reflected in today’s prices. What comes next, no-one truly knows. The key is to remain highly diversified, resolute in the face of any market set-backs and focused on long-term goals.

Risk warnings

This article is distributed for educational purposes and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.