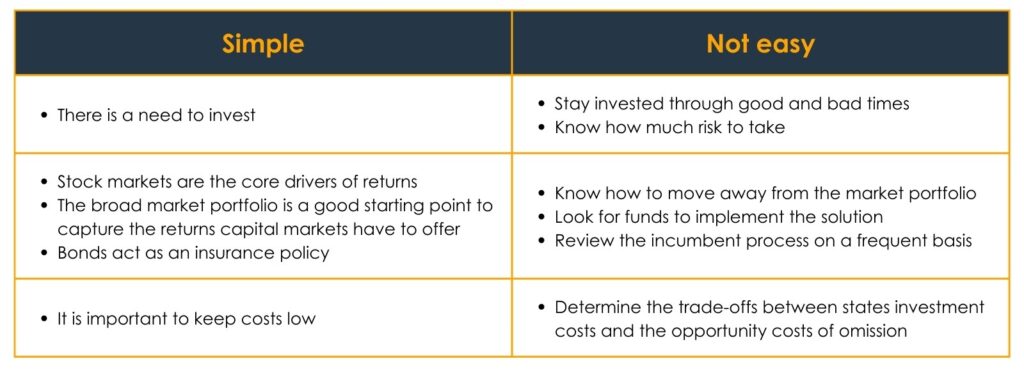

Investing is simple, but not easy

It is a simple statement that the decision to invest in the first place provides an opportunity to protect hard earned savings from inflation, and perhaps grow further. It is not easy, however, to have the foresight, as well as the discipline to deny oneself spending today for the opportunity of a better tomorrow. It is also not easy to work out how much one might want, need and be able to invest in stock markets to help fund future spending goals. Getting this right is key and where good financial advisers can add value.

It is simple that stock markets act as a core driver of returns in an investor’s portfolio, and that a good place to start for stocks is the structure of the global markets, which defines the basic country, sector and company weights and offers broad diversification.

It is also simple that high quality bonds act as protection from economic turmoil and help to smooth returns.

It is, however, not easy to know what evidence to look for in order to gain an understanding about what types of long-term investments typically improve a portfolio’s structure. This comes with the need to build an understanding of the risks one wants to be exposed to through time.

It is also not easy to decide which bonds are deemed to be defensive enough in nature to be considered an insurance policy against the uncertainty inherent in stock markets.

Finally, it is a simple concept that a low-cost fund structured to capture the target strategy gives investors a better chance of achieving their investing goals relative to a high-cost one.

It is, however, not easy to regularly screen for which funds might be best positioned to capture the returns of each part of the market, or to understand the trade-off between the management costs of a fund and the opportunity cost (i.e. what could have been) of omitting an investment. It is harder still to implement a thorough and regular investment oversight process, which is required to maintain confidence in the approach.

Figure 1: Investing can be simple, but that does not mean it is easy to do

Source: Albion Strategic Consulting

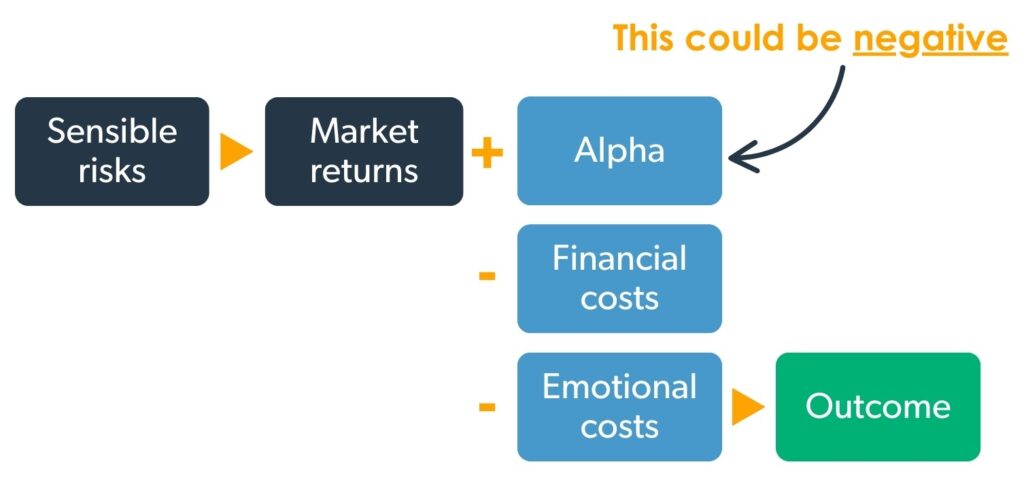

We can consider a simple formula to describe what we expect from an investment outcome, shown in the figure below.

Figure 2: A simple formula to describe an investing outcome

Source: Albion Strategic Consulting

Starting with taking on sensible risks, such as owning a diversified portfolio of investments, we expect a market rate of return.

Depending on how different a portfolio is to the broad market, the portfolio return will come in higher or lower than that of the market. This is what is known in the investment industry as ‘alpha’.

To achieve a return above that of the market portfolio (a positive alpha) an investor must own a portfolio of stocks and bonds that returns higher than the corresponding market. This can be done through picking stocks, timing markets – neither of which are expected to deliver reliably positive outcomes – or it can be more reliably achieved by overweighting areas of the market the academic evidence would suggest reward investors for owning them over the long term, such as tilting to value and smaller companies.

Next, the financial cost of accessing the desired solution is taken away from the outcome achieved. Controlling financial costs makes good sense.

Finally, there is also a cost associated with bad investing behaviour, such as falling foul to biases, illusions or acting on inadequate information. Good process and discipline, as well as having a good financial adviser for additional support, can ensure such a cost is eliminated.

Investing using a well thought-out, evidence-based and systematic investment process helps to reduce the emotional pressures involved and deliver investors with the highest probability of a successful investment outcome. It does not guarantee that the outcome will always be favourable; it cannot, given the uncertainty of the markets. What it does do is to help us make strong, rational decisions and to avoid the silly mistakes that prove to be so costly, so often. In particular, chasing markets and managers in search of market-beating returns and being sucked into the latest investment fad by recent trends, plausible marketing stories and press coverage. Bad process, or a lack of process, has an upside outcome that is down to luck rather than judgement.

Wise words to leave you with

Perhaps reflect a while on these wise words written by Charles D. Ellis in his excellent book ‘Winning the Loser’s Game’ (Ellis, 2002):

‘The hardest work in investing is not intellectual, it’s emotional. Being rational in an emotional environment is not easy. The hardest work is not figuring out the optimal investment policy; it’s sustaining a long-term focus at market highs or market lows and staying committed to a sound investment policy. Holding on to sound investment policy at market highs and market lows in notoriously hard and important work, particularly when Mr. Market always tries to trick you into making changes.’

Simple but not easy. A systematic process and a guiding hand from your adviser are the keys to success.

Risk warnings

This article is distributed for educational purposes only and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Reference to specific products is made only to help make educational points and does not constitute any form or recommendation or advice. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.