The golden illusion

By its very nature, the investing industry is full of differing views on how one ought to invest their hard-earned cash. One of the more polarising debates is whether an investment in gold makes good sense. The debate tends to flare up each time gold experiences a rapid growth in value, such as in the last couple of years.

The pros

Gold has long been prized for its lustre and durability in jewellery, but its uses extend beyond this. As an excellent conductor, highly malleable, stable at high temperatures, and resistant to rust, gold is invaluable in industries like electronics, medicine, and aerospace. Its enduring demand contributes to its value and appeal to investors, as gold has retained purchasing power across centuries. For instance, in gold terms, the pay of a Roman centurion 2,000 years ago is comparable to that of a modern U.S. army captain [1].

Other positives are that gold offers uncorrelated returns to traditional assets such as bonds and equities, providing potential diversification benefits. Many see gold as an ‘Armageddon hedge’, expecting strong returns when faith in the financial system is shaken. Unlike many investment opportunities, gold is a relatively simple concept – being a lump of metal with a market value – and is easily accessed via physical purchase or low-cost open-end funds.

The cons

Gold prices are a function of supply and demand. Investors in gold speculate that others will desire it even more avidly in the future. Unlike traditional asset classes, gold produces no income stream [2], it does not pay dividends and usually costs owners to store and insure it. Many assume its long term expected return to sit somewhere near cash.

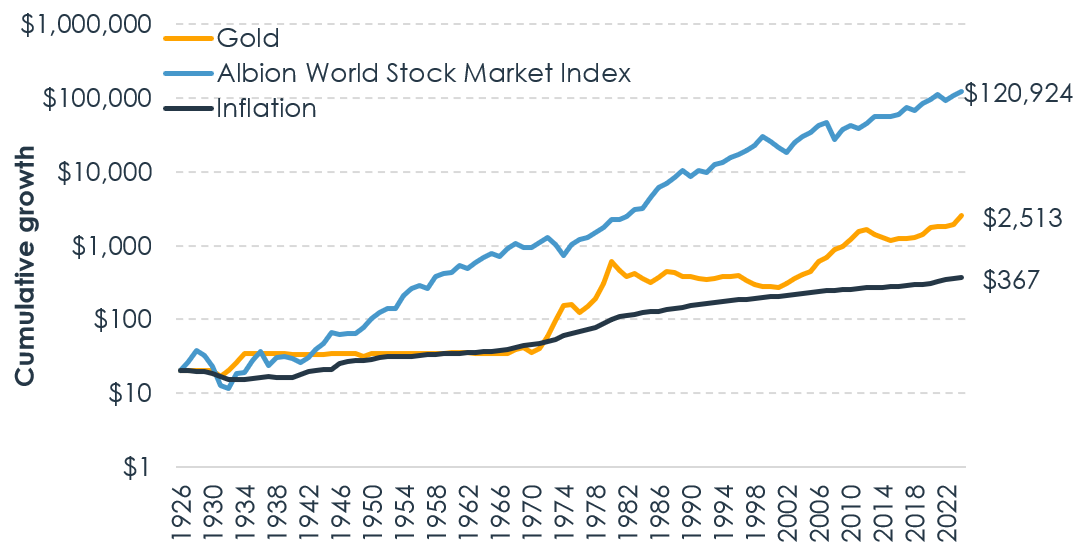

The chart below shows the increase in value of 1 ounce of gold from 1926 to August 2024, rising from around $20 to just over $2,500. Investing the same $20 in global equities during this period would have delivered a substantially superior outcome, nearly 50 times the cumulative gain.

Figure 1: Annual gold spot prices against global equities – 1926-2024

Data source: Gold.org. Inflation: US CPI. Albion World Stock Market Index.

Investors seeking an Armageddon hedge face a dilemma: while many opt for gold-backed funds or ETFs due to the challenges of storing physical gold, relying on the financial system to hedge against its collapse seems contradictory. Owning physical gold has its own issues due to its bulk and other risks such as theft.

Though gold is often promoted as an inflation hedge, the evidence is weak. While it has maintained value over millennia, its performance over more relevant timeframes is less impressive—gold has yet to recover its February 1980 inflation-adjusted high in USD terms and saw an 83% drop in value over the following two decades [3].

The portfolio

Assessing whether gold belongs in your investment portfolio is the job of our investment committee. Each asset class must fill a specific role in your portfolio and is weighed up against the alternatives. In the case of gold, whilst it has some favorable characteristics, superior options exist.

As Warren Buffet succinctly puts it:

“If you own one ounce of gold for eternity, you will still only own one ounce at its end.” – Warren Buffet, 2012

Risk warnings

This article is distributed for educational purposes only and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Reference to specific products is made only to help make educational points and does not constitute any form or recommendation or advice. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.

[1] Erb, Claude B. and Harvey, Campbell R., The Golden Dilemma (May 4, 2013). Available at SSRN: http://ssrn.com/abstract=2078535 or http://dx.doi.org/10.2139/ssrn.2078535

[2] Whilst gold itself does not produce an income stream, financial institutions may try and claw back some of the storage costs through gold lending revenues.

[3] Data source: Gold.org. Inflation: US CPI.